What is the volatility surprise?

The volatility surprise is the only available measure for the impact of monetary policy on the long-term bond market. It captures FOMC announcement induced variation in 30-day expected volatility of the 10-year Treasury yield. You can find detailed information in the paper Zhengyang Chen (2019) “The Long-term Rate and Interest Rate Volatility in Monetary Policy Transmission”. The volatility surprise has three major characteristics that differentiate it from other market sentiment measures.

It reflects the impact of monetary policy on the entire yield curve. The volatility of concern is for the long-term interest rate, instead of for short-term ones. After the 2007-09 financial crisis, monetary policy actions are no longer confined to the federal funds rate target changes but also include forward guidance and large-scale asset purchases programs. All of those tools exert influence on the long end of the yield curve rather than the short end.

It is market-based and does not incur the uncertainty of statistical models. The implied volatility is directly calculated from options prices of 10-year Treasury note futures rather than estimated by any statistical models. It may timely and accurately demonstrate how bond markets react to monetary policy even when there are structural changes.

It is rooted in the risk-taking channel of monetary policy transmission. Borio and Zhu (2012) argue that monetary policy affects financial intermediaries’ risk perception and risk tolerance and, in turn, influences their risk-taking behaviors and real economic outcome. The volatility surprise is a viable measure to indicate monetary-policy-induced changes in risk perception in the financial system.

How does the volatility surprise relate to monetary policy actions?

The volatility surprise bears close relationship not only with conventional monetary policy tool, i.e. the targeting of the federal funds rate, but also with unconventional ones.

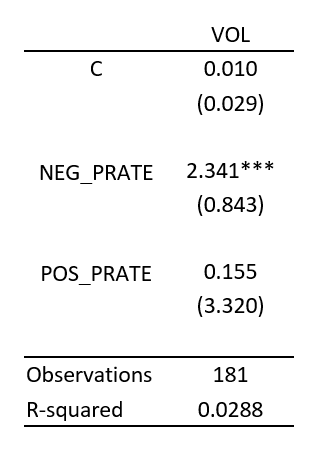

Response of the volatility surprise to unexpected policy rate changes

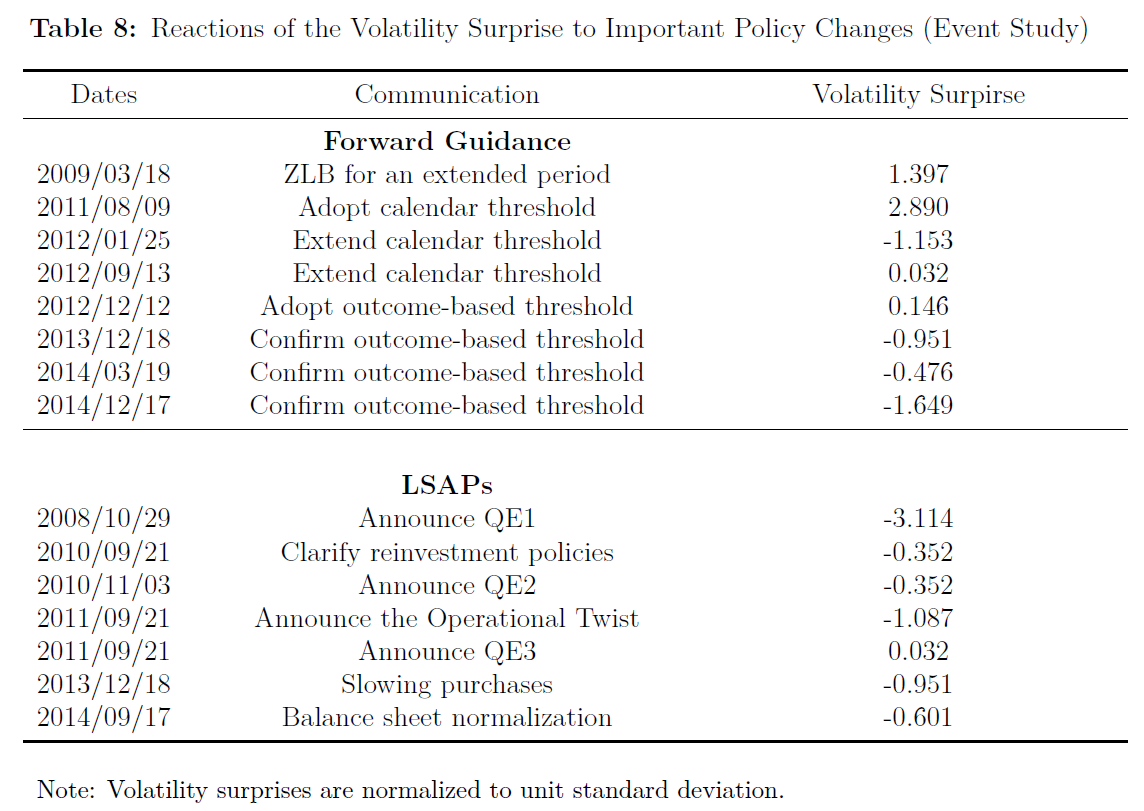

Reaction of the volatility surprise to forward guidance and LSAPs

Latest update for the volatility surprise (1/29/2020)

The reading for the FOMC meeting on 1/29/2020 is 72.61. Detail please refer to the Google Sheet file.